When it comes to purchasing a vehicle, the decision between new and used cars often feels like navigating a winding road with no clear destination. Each option presents its own set of advantages and potential pitfalls, creating a choice that can be as exhilarating as it is daunting. New cars shine with the allure of the latest technology, fresh designs, and manufacturer warranties, while used cars offer the charm of history, affordability, and the potential for unexpected value. As buyers embark on this journey,it’s essential to weigh the pros and cons of both categories thoughtfully. In this article, we’ll explore the key factors that can guide you towards making the right choice for your needs and lifestyle, helping you turn the often-overwhelming car buying experience into an empowered decision. Buckle up; it’s time to drive into the world of new versus used cars!

Evaluating Financial Implications of new and Used cars

When considering the financial implications of purchasing a new or used car,it is essential to evaluate various factors that influence overall cost. New cars typically come with higher price tags, which can lead to larger monthly payments if you finance the purchase.In addition, new vehicles depreciate rapidly—by as much as 20-30% within the first year alone. Beyond the initial purchase price, buyers should account for the following ongoing expenses associated with new cars:

- Insurance premiums: Generally higher for new vehicles.

- Maintenance costs: Initial warranty coverage may mitigate repair expenses.

- Taxes and fees: Greater burden due to the higher value of new cars.

Conversely,used cars tend to provide better value for the money spent and can stretch a budget significantly further. These vehicles have already undergone the bulk of depreciation, allowing buyers to purchase a model that might have previously been out of reach. Financial advantages of used cars include:

- Lower purchase price: Affordability is a importent draw for many families.

- Reduced insurance costs: Generally cheaper than insuring new vehicles.

- Less depreciation: slower value loss over time, making resale easier.

| Factor | New Cars | Used Cars |

|---|---|---|

| Initial Cost | Higher | Lower |

| Insurance Rates | Higher | Lower |

| Depreciation Rate | Fast | slow |

| Maintenance Costs | Higher (initially) | Varies (depends on age/condition) |

Exploring Performance and Reliability Factors

When it comes to purchasing a vehicle,understanding the performance characteristics and reliability of both new and used cars is essential. New cars generally boast the latest technology, higher fuel efficiency, and stricter compliance with emission standards. With advancements in engineering, these vehicles are often designed to maximize performance, providing a smoother driving experience and cutting-edge safety features. Key advantages include:

- Warranty Coverage: New cars typically come with complete warranties that offer protection against manufacturing defects.

- Latest Features: Buyers can enjoy the latest infotainment systems, driver-assistance technologies, and improved handling.

- Better Fuel Economy: New models often utilize more efficient engines and lighter materials that improve overall efficiency.

On the flip side, used cars can deliver remarkable value with lower upfront costs and slower depreciation rates. Though, their performance and reliability largely depend on prior ownership and maintenance history. While some used cars showcase superb reliability, others may require costly repairs shortly after purchase. Below are important considerations for evaluating used cars:

- Maintenance Records: A well-documented service history can provide insights into how well the vehicle has been cared for.

- Pre-Purchase Inspection: Having a trusted mechanic inspect the car can uncover potential issues that might affect reliability.

- market Research: Certain makes and models have a reputation for longevity, making them safer choices in the used market.

| Factor | New Cars | Used Cars |

|---|---|---|

| Cost | Higher initial investment | Lower purchase price |

| Depreciation | Fast, especially in the first year | Slower, less financial loss |

| Reliability | New technology, fewer issues | Varies significantly depending on history |

Understanding Depreciation and Resale Value Trends

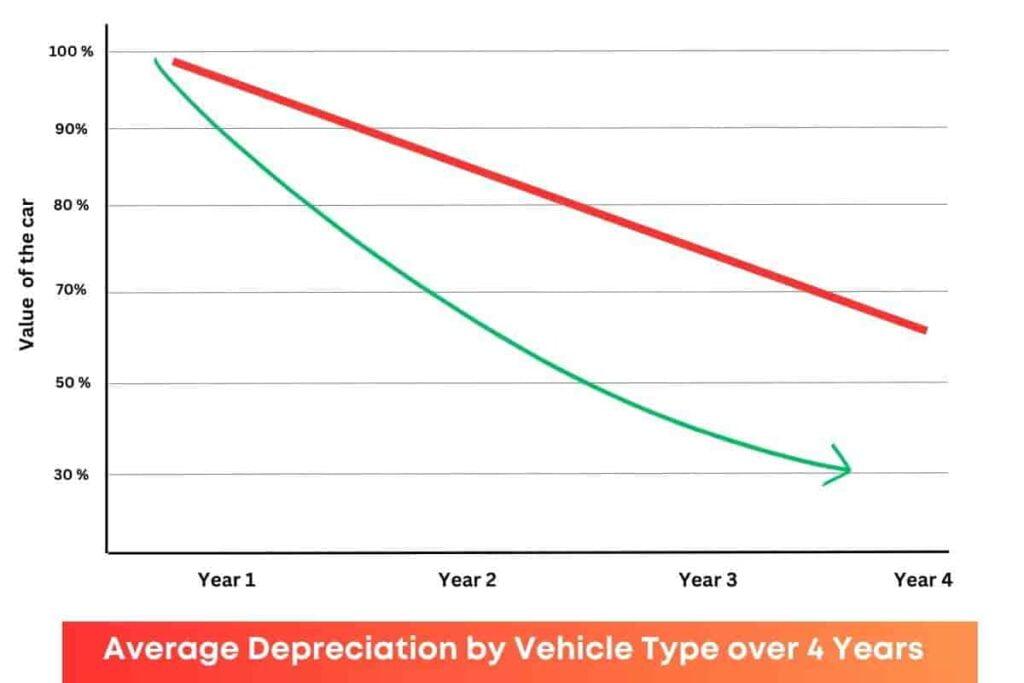

When considering the financial implications of purchasing a car, it’s crucial to grasp the concept of depreciation.New cars lose value faster, with most experiencing significant depreciation within the first few years. In fact, a new vehicle can lose around 20% to 30% of its value as soon as you drive it off the lot. This rapid depreciation could mean that a new car bought for $30,000 might only be worth about $21,000 or $24,000 after just one year. Conversely, used cars have likely already gone through a bulk of this depreciation, making them a more affordable option as their value stabilizes.This means buyers of used cars often get better value for their money without the steep initial loss that accompanies a new purchase.

Another important aspect to consider is the resale value trends of both new and used vehicles. Generally, cars from reputable brands with strong reliability tend to retain their value better than others. Factors such as popularity, demand, model year, and condition significantly influence a car’s resale price. Below is a comparison of trends between new and used cars:

| Car Type | Typical Depreciation Rate (First Year) | Resale value After 5 Years |

|---|---|---|

| New Cars | 20%-30% | 40%-60% of Original Price |

| Used Cars | Depreciation slows significantly | 60%-80% of Original Price |

This table illustrates how new vehicles incur a higher depreciation rate initially, while used cars can often offer a more stable investment with better retention of value over time. When deciding between new and used cars, understanding these trends can be instrumental in making a sound financial decision.

Identifying Lifestyle Needs and Personal Preferences

When considering whether to purchase a new or used car, it’s crucial to assess your unique lifestyle needs and personal preferences. This evaluation will help you better understand how each option aligns with your daily activities and long-term goals. Take into account factors such as:

- Daily Commute: Are you driving long distances regularly or just short trips?

- Family Size: Do you need ample space for family members or gear?

- Tech Preferences: Is having the latest technology and safety features important to you?

- Budget Constraints: What is your financial versatility when it comes to monthly payments and maintenance costs?

These considerations pave the way for making an informed decision. Additionally, think about your lifestyle aspirations and how your vehicle fits into them. Ask yourself:

- Sustainability Goals: Are you leaning towards environmentally pleasant options?

- leisure Activities: Will you require a vehicle capable of accommodating outdoor adventures or hobbies?

- Ownership Experience: Do you prefer a new car’s warranty and reliability or the charm and character of a pre-owned vehicle?

- Resale value: Are you concerned about depreciation and future selling prospects?

The Way Forward

As we rev up to the conclusion of our exploration into the age-old question of new versus used cars, it’s clear that the decision ultimately depends on your unique circumstances, preferences, and financial goals. Each option comes with its own set of advantages and challenges, from the allure of the latest tech and warranties offered by new cars to the value and character often found in used ones.

whether you choose to embrace the scent of fresh upholstery or the charm of a well-loved ride, the key lies in aligning your choice with your personal needs and budget. So, take the time to weigh your options thoughtfully, consider what truly drives you, and remember that the perfect car is the one that fits your lifestyle like a glove. Happy car shopping,and may the road ahead be filled with smooth rides and joyful adventures,no matter which path you choose!